Downgraded

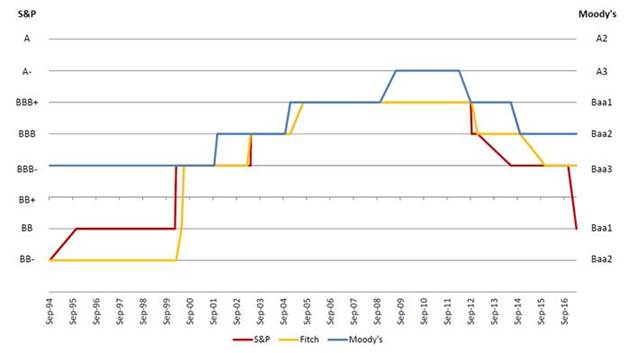

This week , S&P cut South Africa’s long-term foreign currency debt rating to one notch below investment grade. The local currency rating was also cut but remains investment grade. The outlook was kept as negative:

- Long-term foreign currency rating cut to BB+ from BBB-

- Long-term local currency rating cut to BBB- from BBB

Below is a summary of S&P’s statement:

- The downgrade reflects a view that the divisions in the ANC-led government that have led to changes in the executive leadership, including the finance minister, have put policy continuity at risk.

- There is an increased likelihood that economic growth and fiscal outcomes will suffer

- Increasing cost of capital adds further pressure.

- Risks around contingent liabilities were highlighted – expected to be R500bn by 2020. They question the willingness to improve Eskom’s financial position, Sanral and SAA also noted.

- Lowering of investor confidence could stifle investment.

- The pace of economic growth remains a weakness and continues to be negative on a per capita basis.

- They noted credit strengths around monetary policy flexibility and our track record of achieving price stability, as well as the independence of the SARB.

South Africa’s credit rating history

source: Ashburton Investments, S&P, Moody’s, Fitch

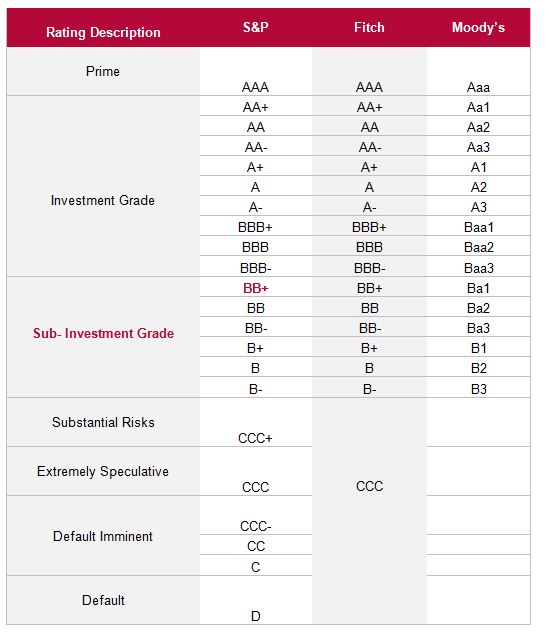

Agency Ratings Tables

While the timing of this move might have come as a surprise, the likelihood of a ratings downgrade was heightened following the recent cabinet reshuffle.

This is clearly negative from SA’s perspective as it results in higher funding costs and fiscal slippage. There will however be no forced selling as SA will not drop out of indices at this stage, but it is clearly a step in the wrong direction. We will watch the other ratings agencies’ responses (Fitch and Moody’s) with great interest.

Prior to these events there was a growing likelihood of short-term interest rate cuts but with the increasingly uncertain outlook this looks somewhat less likely. This all serves to leave the market in an uneasy state. Bond yields have moved up and interest rate sensitive equities have weakened. Investors will be concerned that such moves could ultimately result in weaker economics which in turn will diminish the prospects of interest rate sensitive growth assets.

So how does an investor react to these events? We at Ashburton Investments have long taken the view that there is event risk out there both globally and locally and this latest development would certainly count as that. We look for opportunities but we don’t like to invest in times of extreme unpredictability. While our asset allocation has recently reflected more exposure to growth assets against a backdrop of improving economics, we have still been relatively cautious and conservative. We have emphasised diversification and have a good balance between rand hedge and interest rate sensitive investments. Our focus on quality should also hold us in good stead in these difficult times.

For details on the impact of the S&P ratings downgrade on South African corporate credit portfolios, look out for the Ashburton Credit Insights.

Source : Ashburton Investments