Drawdowns & Downside volatility

Our responsibility to manage client investments with care and diligence is driven by the intention of achieving our client’s investment goals.

Investment goals can only be achieved when a portfolio achieves consistent positive returns that compound over time.

Positive compounding is achieved when the risks that an investment is exposed to are effectively identified and managed. That is why our only purpose and focus is on that which is relevant – to achieve consistent risk adjusted returns.

Any return objective will always be related to a corresponding volatility that the investor will have to be prepared for in order to achieve the desired return objective. We are focused on the management of volatility and to contain volatility within a predicable band.

The advantage of managing volatility is that lower volatility in turbulent times has a smaller drawdown effect on a portfolio. The flipside of this is large drawdowns where negative compounding can have a deteriorating effect on a portfolio. It is our main priority to construct portfolios that deliver consistent returns in any market conditions in order to achieve a positive compounding effect.

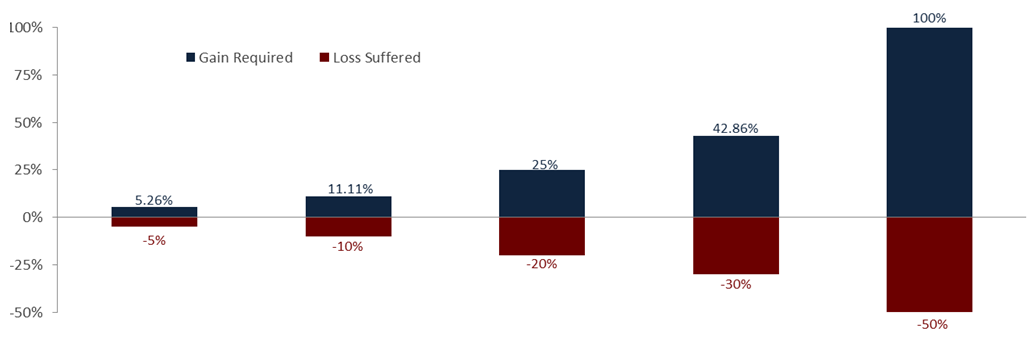

The illustration below highlights the importance of minimising large drawdowns in a portfolio. As illustrated there will always be a need for a greater return once the portfolio suffers a drawdown, just to break even. This negative relationship is even more applicable when the goal of the investment is to achieve positive compounding.

For example consider an investment that suffers a 10% drawdown. For this investment to be restored to the original value before that drawdown, a return of 11.11% is needed. In doing so time will be lost, and time is crucial to create a compounding effect. Therefore the management downside volatility is crucial to prevent permanent loss in value.

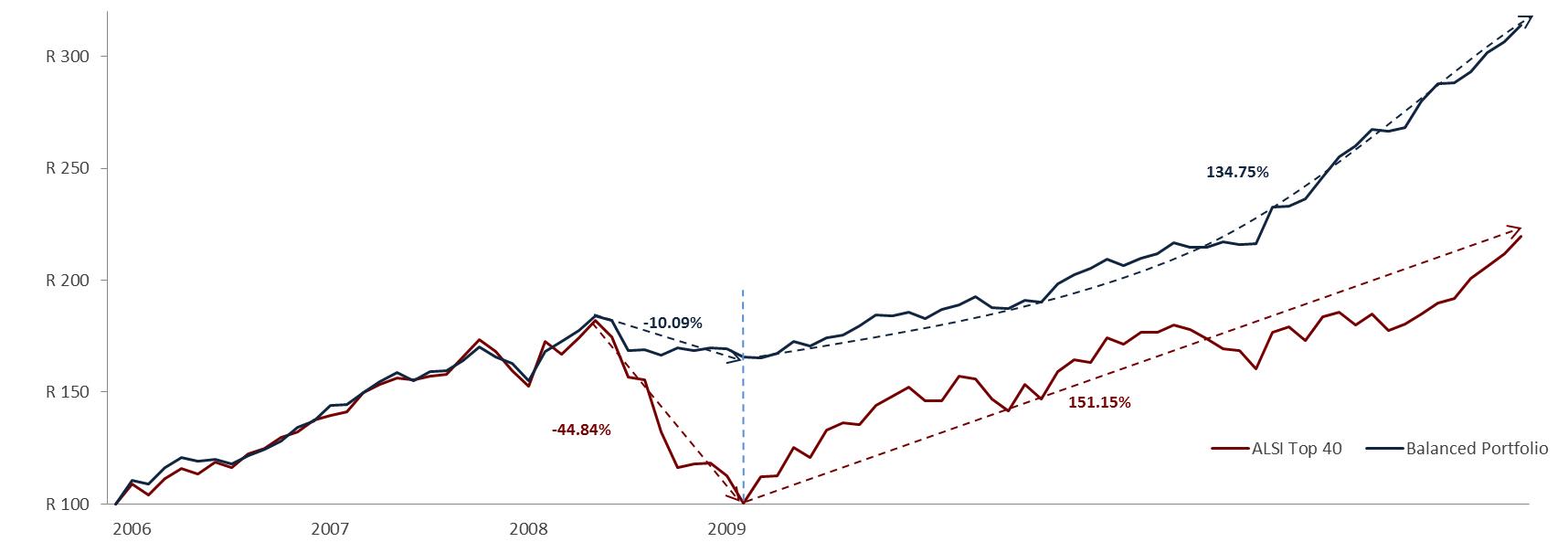

This graph compares the ALSI with our in house balanced portfolio. The Top 40 had a drawdown of 44.84% in 2008 whereas the Balanced portfolio had a drawdown of 10.09%, more than 4 times less what the market portfolio did. The market portfolio returned 151.15% from its lowest point too its highest point whereas the Balanced portfolio returned 134.75% over the same period. Despite this “underperformance”, the only major difference was the higher basis where the Balanced portfolio started compounding from.

We believe that proper down-side management is followed by positive compounding over time and consistent outperformance over the long run as illustrated by the exponential returns of the Balanced portfolio.

Risk can be defined as the probability to lose capital on a permanent basis. There are different risks involved in an investment of which market risk is the most prominent. We manage market risk through diversifying between asset classes and managers. Asset classes differ in terms of their underlying characteristics and this offers diversification benefits.

The way we allocate capital across asset classes are done by making use of different underlying managers with the idea that the combination of managers offers a well-diversified view of different strategies relating to the asset classes invested in. Our manager selection process forms a critical part of our success in the role of custodians that we fulfil for our clients. There is a broad spectrum of managers and as shown by statistics, most active managers do not outperform the market portfolio. That is why we utilise our selection process to assist us in identifying managers that share our focus of managing capital with a risk adjusted mind-set. This process can be regarded as our competitive advantage.

The table on the right illustrates the correlations between the 4 main asset classes as well as a diversified Salvo Balanced portfolio. In terms of risk management, diversification is only effective if the combination of assets, managers and geographies are uncorrelated or have a low-correlation. As illustrated the uncorrelated returns of these asset classes can prove to be useful because returns in a diversified portfolio are not dependant on only one asset class.

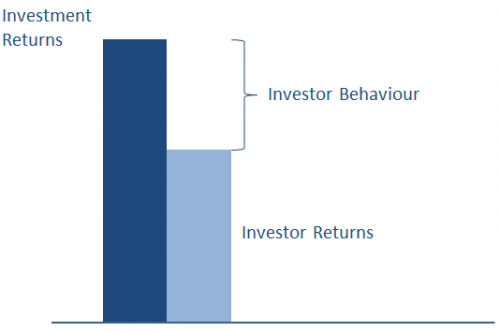

As investment advisors we deem it very important to understand the psyche of our investor clients and to accommodate and manage the potential risk an investor might pose to his own investment. The following important factors summarise our sentiment:

S&P 500 11.81% pa

Average Equity Investor 4.48% pa

The way in which we construct portfolios is to reduce the variability of returns (being more consistent) as that should cause more consistent positive investor behaviour and in the process reduces the risk of negative investor behaviour.

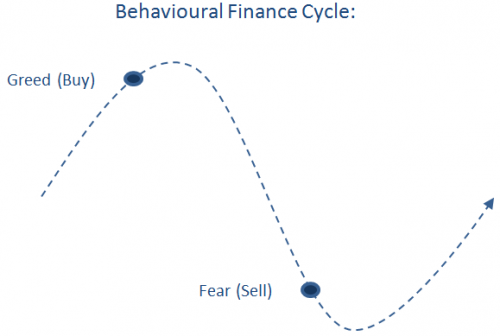

As illustrated on the right, whether markets are falling or rising investors have emotional cycles that have a direct effect on investment returns. For example, in a market that is rising, investors experience optimism or greed-causing an investor to buy. This results in buying at a high.

Then when markets start falling, panic or fear takes hold as a loss in capital is experienced. This fear usually results in selling when prices are low. These emotional states can be detrimental to an investor because opportunities are lost. Loss in opportunities will cause a loss in return. Therefore, as risk is the probability in permanent loss in value, investor behaviour is a risk that an inexperienced investor faces.