Gearing as an Investment Strategy

Gearing strategy

Gearing as a strategy in a portfolio is a way to enhance capital growth. This strategy is effective under the following conditions:

- If the underlying ungeared portfolio consistently manages to outperform the interest rate payable for gearing.

- The underlying portfolio (ungeared) is consistent in the management of its volatility within a predictable band

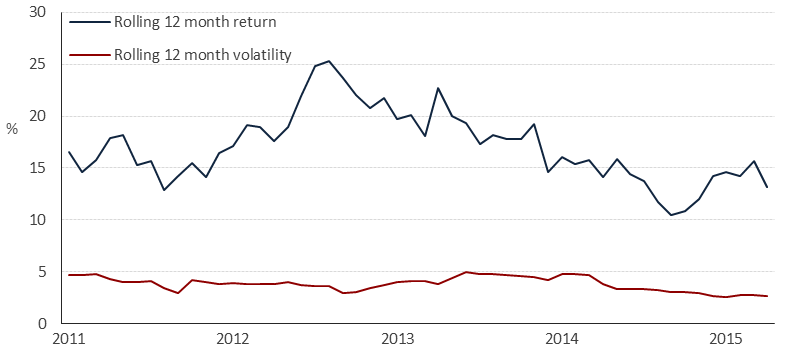

The red line illustrates the rolling 12 month volatility in which the returns were produced. The consistency of last mentioned, qualifies the portfolio to be geared. The above conditions allowed us to advise our clients to gear the Salvo Alternative portfolio. The period since inception until December of 2015 generated a significant additional wealth for our geared clients.

The real test for gearing-how did a simulated geared portfolio do pre and post 2008?

The SARB started to increase rates again in 2015 and it triggered us to revisit our advice on gearing. Given the 3 year history of the portfolio in a low interest rate environment, we decided to do a bit of work on the effect interest rate changes had on the portfolio in the past.

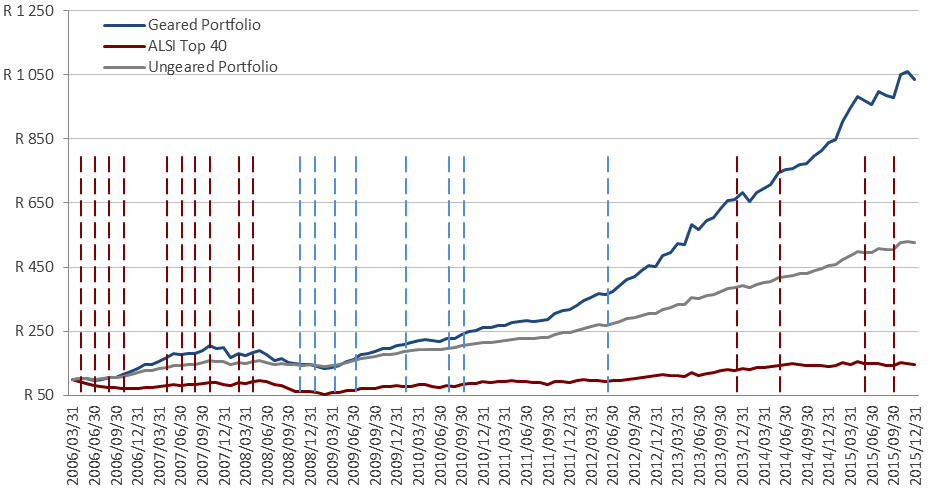

The Salvo Alternative portfolio consist of 7 underlying managers of which 4 of the funds existed pre 2008 and 2 started in 2008 and 1 started after 2008. The simulation below was done with a portfolio that consists of the 3 managers that existed pre 2008 and combined equally in a portfolio that was geared 100%.

The graph below shows the remarkable accumulated growth of a geared simulated hedge fund portfolio benched against the ALSI Top 40 and the ungeared version of the simulated hedge fund. The vertical lines illustrate every interest rate hike (red dotted lines) and cut (blue dotted lines) in the time period from April 2006 to December 2015.

The graph shows than interest rate hikes and cuts had an effect on the hedge portfolios but less so than on the market portfolio. It is as if the advantage to short and hedge is superior to the drag that a higher interest rate have on the geared hedge fund portfolio. Another reason is that the hedge fund portfolio is less sensitive to macro-economic factors than the market portfolio because of its added opportunity spectrum. The result of last mentioned is best illustrated in the way the hedge fund portfolios handled the crisis period of 2008 compared to the market portfolio (see graph below)

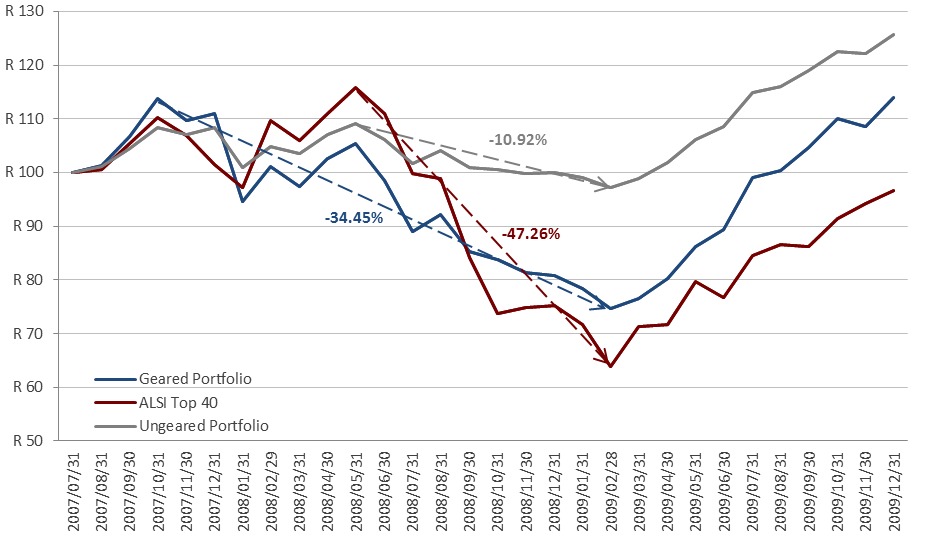

- This chart emphasise the attractiveness of investing in a well-constructed Alternative portfolio especially in a time of chaos like in 2008. The geared portfolio was 34.45% under- water whilst the market portfolio had a drawdown of 47%

- It is interesting to note that the geared portfolio drawdown consisted of only 22% caused by the underlying portfolio (-10.92% x 2) and the rest was caused by an average interest rate over the underwater period of 12.61% pa. That means the average prime interest rate in this time was 12.61% + 1% = 13.61%. It is our opinion that the probability for prime to reach these levels again in the next 3 years are quite slim given the lack of growth in the global economy at the moment.

- It took the geared portfolio 26 months to get out of the underwater period versus the 45 months of the market portfolio. The smaller draw down and higher velocity to get out of the underwater position must be the single most important dynamic that caused the massive outperformance that followed.

Conclusion

- When markets are in crisis globally one should stick to the gearing strategy as the real value is only realised after the crisis and the recovery come in a short time period

- As an investor who utilise gearing as a strategy you need to be comfortable with drawdowns as discussed above. This draw down should be less than the market portfolio.

- Gearing as a strategy to increase capital growth is an attractive proposition from a return point of view given that drawdowns can be stomached by the investor

- A geared hedge fund portfolio is suitable for a moderate to aggressive investor

- Interest rates seems to have a minimal impact on the decision to gear or not to gear as the simulated geared portfolio performed well above average when interest rates were at its highest (2009-2010).