We take a look back

In this post, we look back at the year’s performance of the various asset

classes and highlight one of the most statistically significant observations (mean reversion) in financial markets and how it can benefit you as a

long-term investor.

The most important quality for an investor is temperament, not intellect

– Warren Buffet

Growth Assets Continue Poor Performance

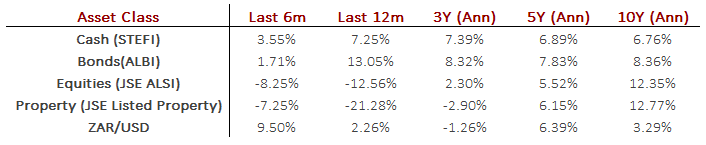

Following up on the previous newsletter, things seem as if it went from bad to worse towards the end of the year. At the end of October 2018, we observed the JSE All Share Price Index’s first negative 36-month return figure since November 2010. This highlights just how difficult the last 3 to 5 years have been for growth assets. Below is a summary of returns for the relevant asset classes:

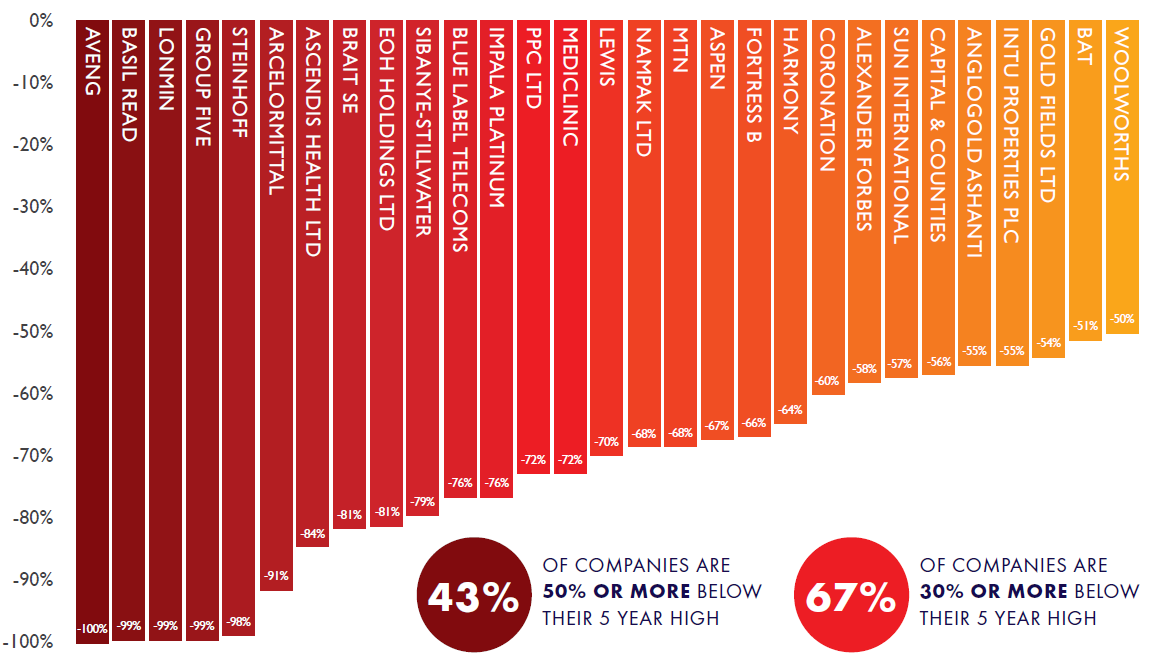

Investors are no doubt disappointed that, on average, equities could not outperform cash over 5 years. It is only over the longer term that Equities have been able to reward risk-tolerant investors. To understand just how difficult equity investments have been, research was done on our local equity market and found the following:

This clearly shows that equities (which includes high-quality companies) experienced sharp sell-offs, whilst most active investment managers also struggled to successfully navigate risk markets during 2018.

Although there are very good reasons for the recent volatility in our market (such as the threat of international trade wars, populist movements that are creating uncertainty and weak domestic economic data) investors want answers and most investors truly do need returns. This environment and lack of inflation-beating returns (in the short-term) causes important behavioral biases to come to the fore in the decision making of investors. Two of these behavioral biases are discussed below:

• Loss aversion – refers to the fear of losing capital. This fear leads to a withdrawal of capital at the worst possible time. This is known as “panic selling”. This often occurs when short-term volatility increases. As markets revert to the long-term average many investors panic and see the correction is the market as a “crash” and exit all their positions, thereby realising (monetising) a negative return instead of sticking to the long-term investment strategy.

• Recency Bias – This occurs when investors overemphasise recent events when making decisions. For example, people tend to favor equities after the market has had a strong upward trend and tend to avoid them after a downturn. This often leads to “buying high and selling low,” which is contrary to the mantra for successful investing.

Both of these biases affect the probability of achieving your desired investment outcome if it is acted upon. Research also shows that investors tend to “lock in” bad performance when markets are negative. We believe that if investors are able to understand the way markets work, they may tend to exhibit the attributes of successful investors who have been able to overcome these biases.

One of the key characteristics of markets is mean reversion. If you as an investor understand mean reversion, you may start to see opportunity during tumultuous times.

What is Mean Reversion?

Without getting into the quantitative definition of the term, mean reversion refers to the HIGH and the LOW periods of returns returning to the long-term AVERAGE (or mean). In other words, periods of ABOVE-AVERAGE performance are usually followed by a “correction” or “reversion” to the average and periods of BELOW-AVERAGE performance is also generally followed by a period of better performance towards the average (it is pretty much the definition of volatility if you think about it and that is exactly why volatility is needed to cause mean reversion to take place).

“Mean reversion is not only mathematically true (it has to be, in fact) but it can be used to good effect by investors. Because variables often take a long time to revert, it provides time and opportunity to take advantage of mispricing evident in the market.”

– Dave Foord

Evidence of mean reversion in our market

Mean reversion is evident in almost all financial and quantitative data. Whether it be Interest Rates, Inflation, Trading Multiples, Business Cycles, GDP, Returns etc.

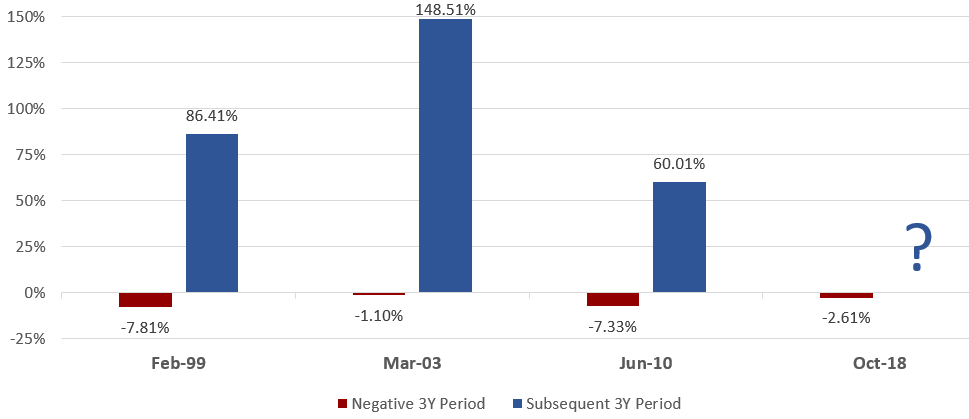

As mentioned earlier, at the end of October the JSE All Share Price Index returned its first negative 3-year period since November 2010. We analysed all of the 3-year negative return periods since 1995 to see whether or not mean reversion occurs as we believe it should, i.e. after a negative 3-year period we expect to see a subsequent 3 year period of positive performance. As seen below mean reversion occurred as expected (return period ending Nov 2018)*:

We know that it would be foolish to base long-term forecasts on historical data, however, in the case of mean reversion it has been statistically significant in the past. The duration of the negative period is always unknown and can even take a few months to return to positive territory, however, the evidence of mean reversion in returns is clear.

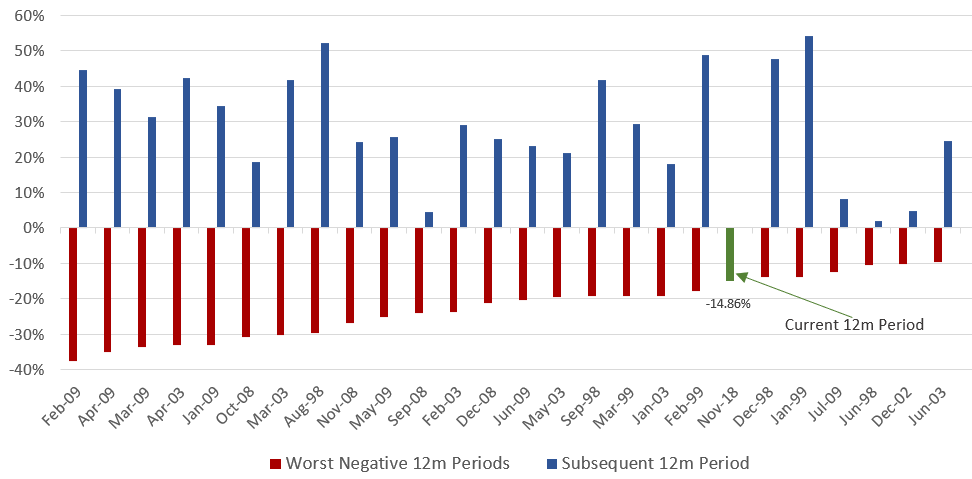

Another example of mean reversion is to take a look at shorter time periods. We analysed the worst 12m periods of return and looked at the subsequent 12m performance. The results were similar:

Once again mean reversion was statistically significant for levels lower than 9% over a 12m period*.

Conclusion

As investors alongside our clients, we understand the frustration that you are experiencing. We encourage our clients to remain disciplined and avoid making irrational decisions if there is evidence to suggest that returns mean revert from disappointing levels.

If your investment objective has not changed in the last 12 months try to see the bigger picture, the long term picture and study the behavior of succesful investors during difficult times. Salvo Capital appreciates all the support and trust shown in our capabilities and processes to manage client capital. We are constantly positioning client portfolios in order to capture returns and effectively manage the risk that is needed to do so.

Kind Regards

The Salvo Capital Team