Times may be tough

…but don’t cancel your life cover!

Many South African households are feeling the pinch financially, and you may be tempted to cancel your life cover to free up some much-needed cash. But this could be a big mistake, with dire financial consequences for your loved ones.

did you know that about 380 families loose a breadwinner everyday in South Africa

Hennie de Villiers, the deputy chairman of the life and risk board committee at the Association for Savings & Investment South Africa, says it may be impossible to replace your life cover as you grow older.

If you are struggling to make ends meet, the temptation to let go of your life cover can be overwhelming. But before you do, weigh up the expense of your monthly premium against the dire financial impact the loss of your income could have on your family. Actuarial modelling shows that about 380 families lose a breadwinner every day in South Africa, yet the lapse rate of life policies – when a policyholder stops paying premiums and loses his or her cover – is high.

Looking back

In 2016 – over two million risk policies, covering events such as death, disability and dread disease, were lapsed within their first year. Although this is a decrease from the nearly 2.2 million risk policies lapsed in their first year in 2015, the fact remains that South Africans are critically underinsured.

Of the more than 720 000 life policies at Liberty Life, about 60 000 (between 8% and 10%) lapse each year. The main reason (over 90%) for lapses is affordability. Most policies (50%) were lapsed by young and middle-aged parents, followed by young single people who are at the beginning of their careers (25%).

The way forward

This is a grave concern. Families under severe financial pressure prioritise loan repayments, school fees and other important expenses over life assurance premiums. The problem with this is that you can’t predict when cover will be needed.

Cancelling it is a massive risk.

You may think you can simply cancel your life assurance now and reinstate it in the future when you’re out of the woods financially. The problem with taking out cover when you are older, is that your premiums are likely to be substantially higher, serious health conditions may be excluded from the cover, or you may even be uninsurable. A general rule of thumb is that life cover is generally much cheaper when you are younger and healthier.

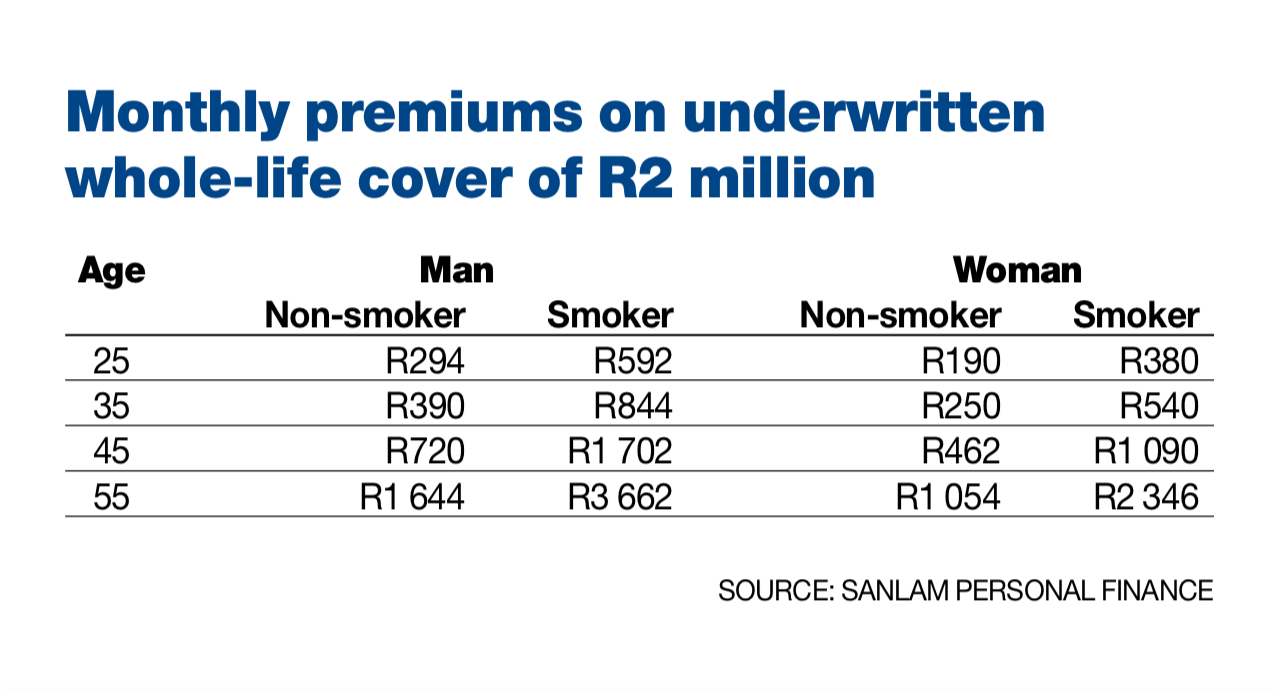

As an example, a healthy, non-smoking 25-year-old man could qualify for R2 million of life cover at a monthly premium of R294. A healthy, non-smoking woman of the same age would pay as little as R190 a month for the same amount of cover. With a level premium pattern, the cost of this cover should remain the same for the rest of their lives, even if they developed serious illnesses later in life.

(Life assurers also offer an escalating premium pattern that has a lower premium initially, but the premiums become more expensive as you get older, until they may be unaffordable.)

The table below shows the cost implications if you cancel your life cover and reapply for the same amount of cover later in life. At the age of 45, the cover costs double what it costs at age 25.

“It is also important to note that if you are diagnosed with a health condition such as diabetes or cancer before you apply again, some companies may refuse to cover you,” De Villiers says. “Others may place exclusions and limitations on your policy, refusing to pay out if you die of the particular condition. Alternatively, they could load your premiums, making the cost of your cover more expensive relative to other people your age.”

He warns that if you skip only a few premiums, you may have to undergo the underwriting procedure all over again, and your life assurer may take any deterioration in your health into account when considering whether or not to reinstate your policy and what premiums to charge.“If you miss a premium payment, you need to contact your life company as quickly as possible to make alternative payment arrangements and reinstate your cover,” De Villiers says.

ALTERNATIVES TO DITCHING YOUR COVER

There are a number of alternatives you should consider before you cancel your life cover, these include:

• Reducing your monthly expenses. Critically evaluate your monthly budget and cut back on non-essential expenses, such as your satellite television subscription. Be realistic about wants versus needs.

• Renegotiating your debts. You could approach your bank and creditors to negotiate the terms of your debt repayments. Your creditors may be willing to accept smaller monthly repayments over a longer period. You could also consider debt consolidation, or approach a debt counsellor for help.

• Pausing your savings. You could temporarily halt your contributions to a unit trust portfolio, or take a “payment holiday” from your endowment policies or retirement annuities (but first make sure you won’t pay any penalties if you do). Stop saving for short- and medium-term goals, such as a holiday or buying a house, before you stop saving for retirement.

• Streamlining your short-term insurance. Insurance on your home and vehicle is important, but you could reconsider whether you need comprehensive all-risk cover that may include your jewellery and mobile phone, for instance. You could also reduce or cancel add-on cover, such as cover for your car sound system.

• Negotiating your premium payment pattern. If you recently purchased level-premium life cover, you could request to change to an escalating-premium pattern where your initial premiums will be lower and increase over time. This would enable you to keep the same amount of cover, while giving you some short-term financial relief. You may be asked to undergo medical underwriting before the assurer will make these changes.

The best way to deal with financial problems is to acknowledge that you need help and consult a professional financial adviser.

A Professional will be able to examine your financial situation objectively and guide you on making the best decisions appropriate to your individual needs.

source: iol