Newsletter

The end of February sees an end to another tax year.

In this newsletter, we remind our clients that the current tax year is almost coming to an end, and as such the benefits of topping up or starting a Retirement Annuity will be discussed. We’ll also review the structure and the long-term benefits of investing in a Retirement Annuity.

What is a Retirement Annuity?

As mentioned in the name, an RA (Retirement Annuity) is an investment vehicle that allows any investor in their personal capacity, to save for retirement. The following rules are applicable to this investment vehicle –

- Investment contributions can be made by a lump sum investment or on a monthly basis. These amounts can start from a minimum of R500 per month or a lump sum of R10 000. The entire contribution can be deducted from your taxable income up to certain limits which will be discussed later.

- The underlying investment must be made in accordance with “Regulation 28”. This is a rule issued under the Pension Fund Act which limits the investor’s exposure in particular assets/asset classes. Currently, this rule limits offshore exposure to 30%; 25% in listed property and a total of 75% in listed equities.

- Investors can only access invested capital on retirement after age 55. Invested capital cannot be withdrawn (except under specific circumstances). On retirement, a maximum of 1/3rd of the capital is available as a lump sum to the client (subject to tax tables).

Tax Benefits

An RA provides great tax benefits to investors. These benefits are actual “Rand & Cent” savings (when compared to discretionary investments). These savings are allowed to compound over the term of the investment which can have substantial benefits to investors. So what exactly are the tax benefits and why is it important to know?

1. You pay NO tax on your investment’s returns

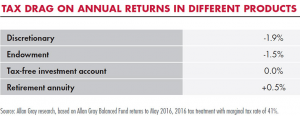

All investment returns return to the investor and no return that is earned is taxed. This means that all local and offshore interest, dividends and capital gains earned accrues to the investor. This can have a massive impact on the long term return to the client. The table below illustrates the impact of tax based on a 10-year investment in the Allan Gray Balanced Fund across different investment vehicles.

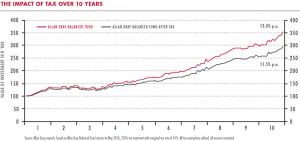

This difference in return will have a large impact on the future value of the investment. Below is a graph that illustrates the 10-year impact that such a difference in return can make. If 100 was invested in the same fund for 10 years and the only difference is the investment vehicle being a retirement annuity and a unit trust.

This is a good reason to consider using a Retirement Annuity as a long-term investment vehicle.

2. Contributions are deducted from your taxable income which lowers your tax bill.

One of the benefits of investing in an RA is the generous tax deduction for contributions, subject to a maximum of 27.5% of the greater of your taxable income with an annual ceiling of R350 000. The best way to illustrate the benefit is by means of an example.

Adam earns an annual salary of R300 000. He has contributed 15% (R45 000) of his annual salary to his RA this year. On learning about the benefits of maximising the tax breaks offered to retirement savers, Adam decides to make an additional contribution to his RA. He has been disciplined throughout the year and decides to use the money he has saved to maximise the 27.5% tax benefit before the end of February. He contributes an additional R37 500 (an additional 12.5% of his annual salary) on top of the R45 000 he has already contributed. Adam can expect to receive R9 750 from SARS when he files his tax return.

This example shows that the government encourages us to save for our future now by ensuring our take-home pay doesn’t decrease in line with the amount we save for retirement. Below is a table, which calculates the monthly tax due for an individual earning R300 000 per year (R25 000 per month), at different RA Contribution levels. Note that as your contribution levels go up, more money is invested in your RA and less goes to the tax man.

Compared to someone earning the amount per year but not investing the full allowance, the investor in an RA investing 27.5% of his/her income will have paid R21 623.40 less tax and have invested R82 500 throughout the year towards retirement in a product that will earn tax-free returns.

Conclusion

You have until the 26th of February 2019 to top-up your Retirement Annuity or to open a new investment.

We encourage investors not to only invest with a tax-break in mind but also to consider the long term impact of a sound and prudent investment decision such as this. If you are interested or have any other questions you can contact your financial advisor at Salvo Capital.

If you are planning to make use of these tax concessions, you will need to do so well in advance of the 28 February deadline to allow time for your investment manager to process your investment.