The 100 year Life

Don’t just plan for retirement, Plan for a long life

Those in the retirement industry bemoan the fact that South Africans are poor savers and are often one emergency away from trashing what savings they have.

A survey shows that just one in three ‘baby boomers’ has any form of formal retirement saving.

There are a few immutable truths about retirement savings that are often overlooked:

- Start early and put 15% into retirement savings as soon as you start working.

- Worry less about which investment house is managing your money than the end goal of maintaining a decent standard of living when you retire.

- Never touch your retirement savings for any reason, not even emergencies.

- Plan for a long life, well beyond the retirement age of 65.

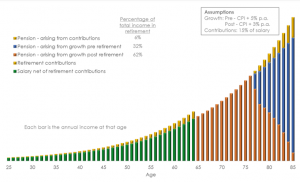

The graph below illustrates what happens when you invest 15% of your earnings from the age of 25 and keep this going throughout your life, while earning a suitable level of investment return.

The bars in the graph show the person’s income throughout their working, as well as their retired, lifetime. The eye-opening insight from the graph is revealed by breaking down where the pension amounts actually come from, as summarised in the table on the left. The amount you will spend in your whole retirement is derived from three sources – (1) the contributions you make, (2) the growth on those contributions up to retirement date and (3) the growth on your investment post-retirement, i.e. when you are drawing out your pension.

That’s the power of investing for the long term and letting compound interest do its thing.

A mere 6% of your retirement money comes from the contributions you made while working – the remaining 94% is generated from returns, of which only one third was generated before retirement. A massive two thirds was earned while you were retired. This assumes that you are earning a market return of 5% above inflation in the years prior to retirement, and 3% above inflation post retirement.

That’s the power of investing for the long term and letting compound interest do its thing. The contributions you make as a proportion of your retirement pot are minute when measured over the long term, but you have to make them early. This also shows how important the post-retirement phase is and hence how important your decisions are in relation to the annuity you use.

Saving for retirement is simple but it isn’t easy.

There’s no easy way around this, “We focus on getting people to have a retirement plan in place so they don’t get distracted by fads and get-rich-quick schemes that are supposed to get you there faster. The main thing is to have patience. People want to see quick returns, and this lack of patience can be disastrous. If they save R1 000 a month and at the end of the year they see just R12 500, they start to question why they are putting in all that effort for such little return. But it’s import to stick to your plan and remember why you started in order to see the returns further down the road.”

Three main reasons for saving

Three major reasons for people to save:

- Retirement (not preserving savings when changing jobs is a problem, even if used to pay off debt)

- Emergencies

- Education for children (if applicable).

We recommend that our clients make sure all three of these needs are met in one’s financial plan and that the savings are appropriately segregated. This is to ensure that any emergencies that arise do not eat into the retirement or education funds. Many people save diligently for retirement until an emergency arises, then cannibalise their retirement funds. Although this is better than borrowing to handle an emergency, it isn’t advised because it’s so difficult to catch up on retirement savings when they’ve been used for other purposes.

“It is preferable to have separate, short-term savings to deal with emergencies, and to never allow anything to start eating away at your retirement savings.”

Big-impact decisions

Retirement fund trustees spend a lot of time choosing asset managers and deliberating whether to change managers if they have a period of under-performance. In terms of the impact on eventual retirement outcomes for members, this isn’t the most impactful decision. Trustees need to identify which decisions are the most impactful and spend their time accordingly.

Spending time understanding the objectives, setting (and encouraging) appropriate contribution levels, assisting to make preservation simple for members who leave, excellent communication to members and ensuring that the investment strategy is designed to deliver superior long-term growth by having appropriate levels of growth assets (i.e. the asset allocation decision) are all more impactful decisions than deciding over exactly which asset manager to invest with. This is always also certainly more valuable to members than switching back and forth between managers based on trying to be invested with the best performing manager.

The same can be said for trying to decide between active and passive investments. It’s far more important to ensure that you are paying a reasonable fee for the type of portfolio you have selected and then staying put for the long term. Once again, patience is important. Switching between different styles or different managers is likely to destroy wealth for members.

Conclusion

Saving for retirement is simple but it isn’t easy.

As a trustee, you can help members by focusing on the decisions that have the most impact on their retirement outcomes.

As a member, it’s important to take responsibility for your retirement plan and have the discipline to execute it, the patience to let compound interest work its magic and the resilience to sit tight when the ride gets bumpy.

Don’t just plan for retirement, plan for a long life

source : Moneyweb